Related Articles

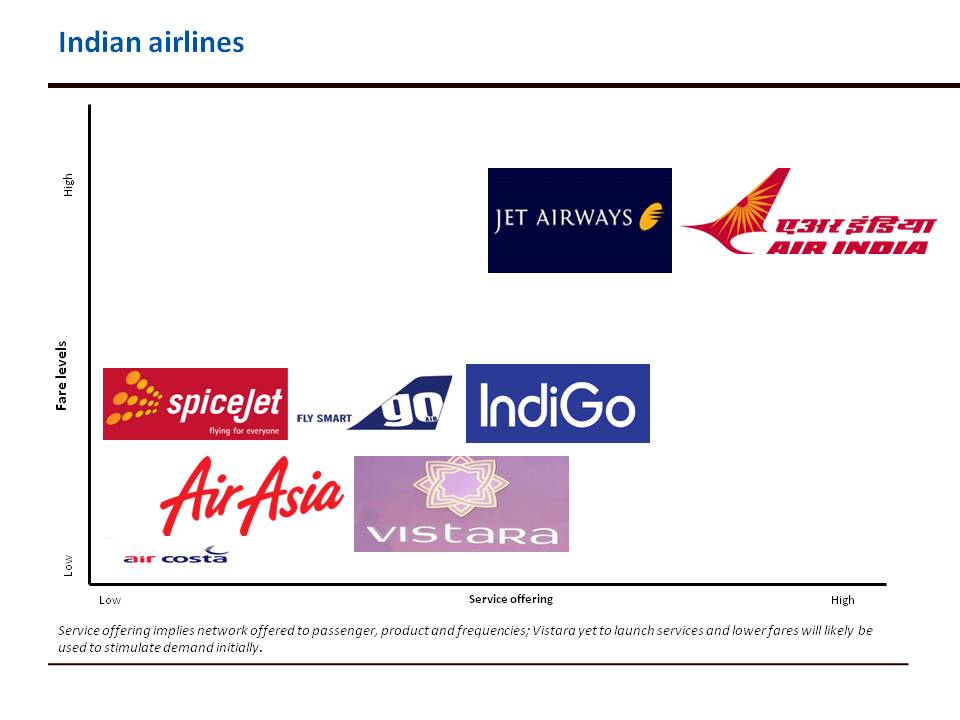

The Indian skies are fairly busy. With seven airlines operating, one about to launch services, one in a bit of a challenge and six airline licenses granted by the Ministry of Civil aviation, increased competition is inevitable. Yet, if one looks at profitability, there is only one airline that has been consistently profitable. Which begs the question, are all the airlines offering the same product and just competing on price or are there subtle differences? How are the airlines positioning themselves? When comparing service offerings and fare levels, the current positioning of the airlines is as below:

Air Asia and Air Costa have positioned themselves in the ultra low-cost segment and are actually stimulating demand. The three low cost carriers Spicejet, Go Air and IndiGo in terms of fare offerings are very close to each other but in terms of service levels Indigo due to its wider network, frequencies and product is positioned higher. Vistara though attempting to capture the premium segment, initially is placed lower as it will likely have to resort to discounting to capture demand initially; and Jet Airways and Air India are positioned as full service carriers with higher fare levels.

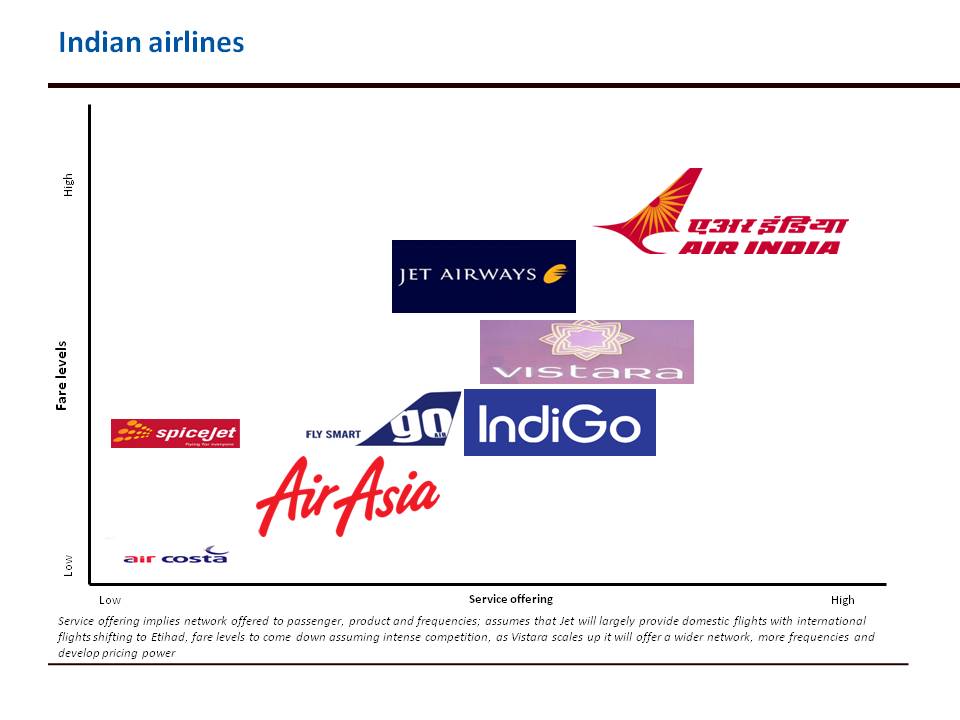

As one looks out two to five years out (though in the airline business one can never be certain), the positioning is likely to change as some carriers mature and grow their network while others start adapting to present day changes in business models. The anticipated positioning as it would evolve in a two to five year period is as below:

Air Asia as it scales up would have an increased service offering in terms of additional cities on the network. Indigo and Vistara would likely compete to capture a similar segment (assumes that Indigo would deviate a bit from the current business model and introduce a premium cabin on some sectors); Jet would likely operate a network with a focus domestic operations and with pared down international operations (which points to the fact that Jets operations would largely provide feed) while Air India would continue to have a relatively higher service offering and correspondingly higher fare levels.

That said, with the Indian market being as price sensitive as it is, low fares would continue to drive demand. Yet, as the travelling public matures, it is likely that at least a portion of the travel demand (albeit a small portion) could start to switch carriers on criteria other than price. As and when that happens this segmentation between carriers would be more pronounced and if low cost airports are thrown into the mix, it would further help this segmentation.

Either way it works out, the next few years – at least for the travelling public and aviation enthusiasts – should be interesting, dynamic and perhaps a tad bit confusing.

In many cases fares on Indigo are equal to or higher than full service carriers like Jet and Air India. Many companies allow their employees to travel on full service carriers but their employees still book on Indigo. The major reason many travelers (especially business travel) prefer Indigo is reliability in terms of on time schedules and frequency of their flights.

Vistara stands to capture a good share of this traffic if and only IF they manage to be reliable from the get go. If they lose their standing in the market in the beginning they will find a very hard time convincing the business crowd to give them another chance.

Positioning – in the mind of the customer, is not necessarily the same as the airlines strive to position themselves. From the bulk Indian customers’ PoV, (1) timing and connection, (2) cost and (3) reliability are the 3 most important parameters than whether the carrier is LC or full-service. This LCC-full service categorization seems to be a non-issue and rather irrelevant to the customer.

I think previous MoCA explained this very well

Vistara – Premium FSC

Jet Airways – International Feeder FSC

Indigo/Air Asia/GoAir/SpiceJet – LCCs

Air India – Serve left over segments.

Since Indian domestic market is capitalized by Indigo, Goair and other LCCs..AI and Jet should concentrate more on Intl markets. AI should open new routes in Africa,South East Asia, Europe and North America. Pity that no Indian carrier fly to Africa where there is lot of passenger movements between 2 continents for medical and business purposes. AI have good back backup from the Govt now and Star Alliance. With Vistara and another few new entrants coming into the market AI should cut down loss making domestic routes and increase capacity to Middle east and SEA where Indians travel more. Indigo’s aggressive growth clearly shows they want to evict all their competitors and play a monopoly in the domestic market. I wish the AI management focus more on exploring new intl routes and use DEL well as a Hub!!