Related Articles

SpiceJet has seen challenging times over the past 5 years. While numerous reasons can be cited for this ranging from network structure, fleet decisions, competition, ability to command a premium, management churn, market weakness and overall brand strength, the financial position of the airline as of today is quite challenging. Much is being reported about the possible funds infusion and/or recapitalization of SpiceJet. This note only examines the financial position with a few strategic points.

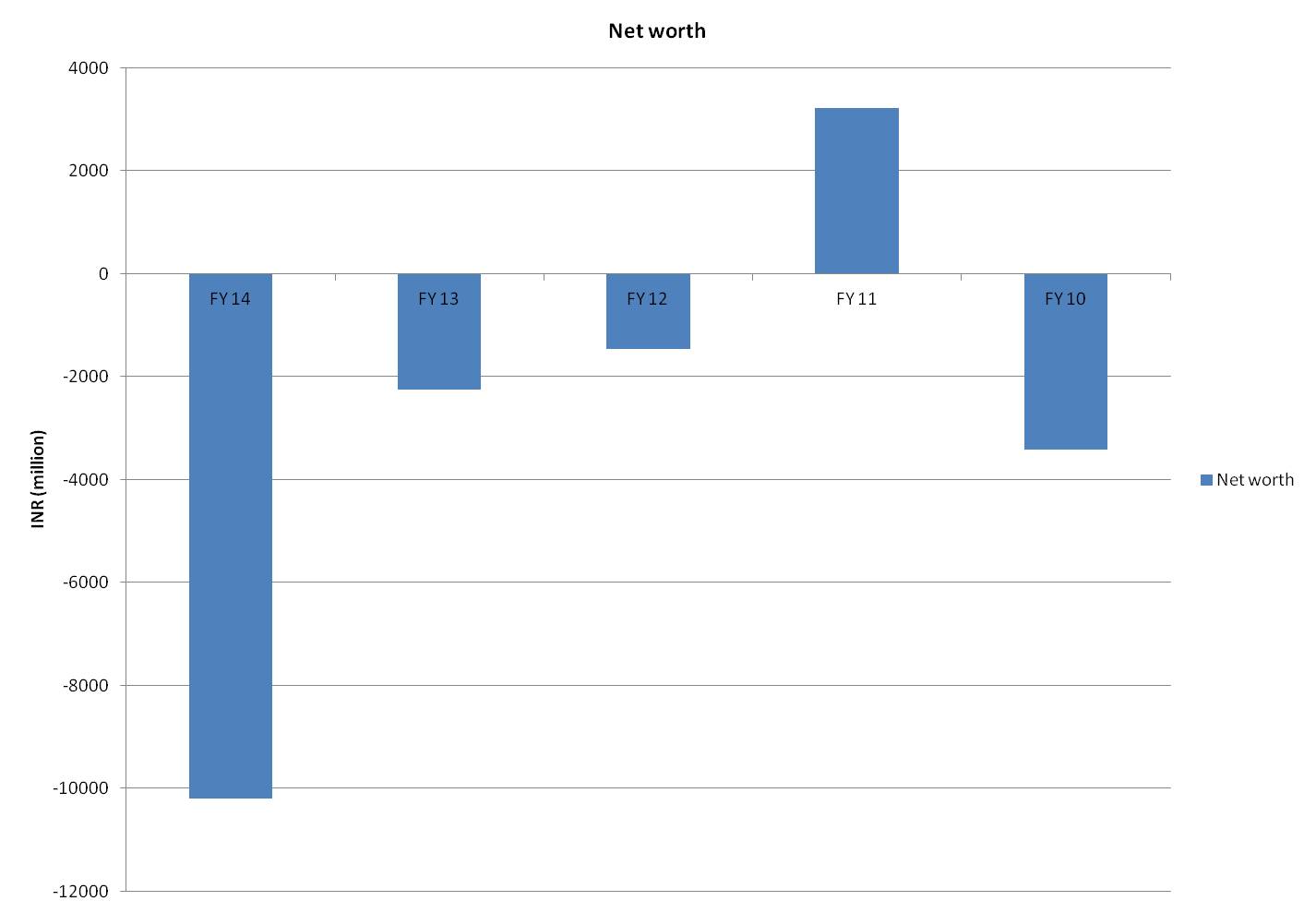

Net Worth

Spicejet’s net worth has decreased significantly over the past 5 years. In other words, its liabilities exceed its assets, thus any recapitalization would need significant returns for the investment to yield good results.

Debt Levels

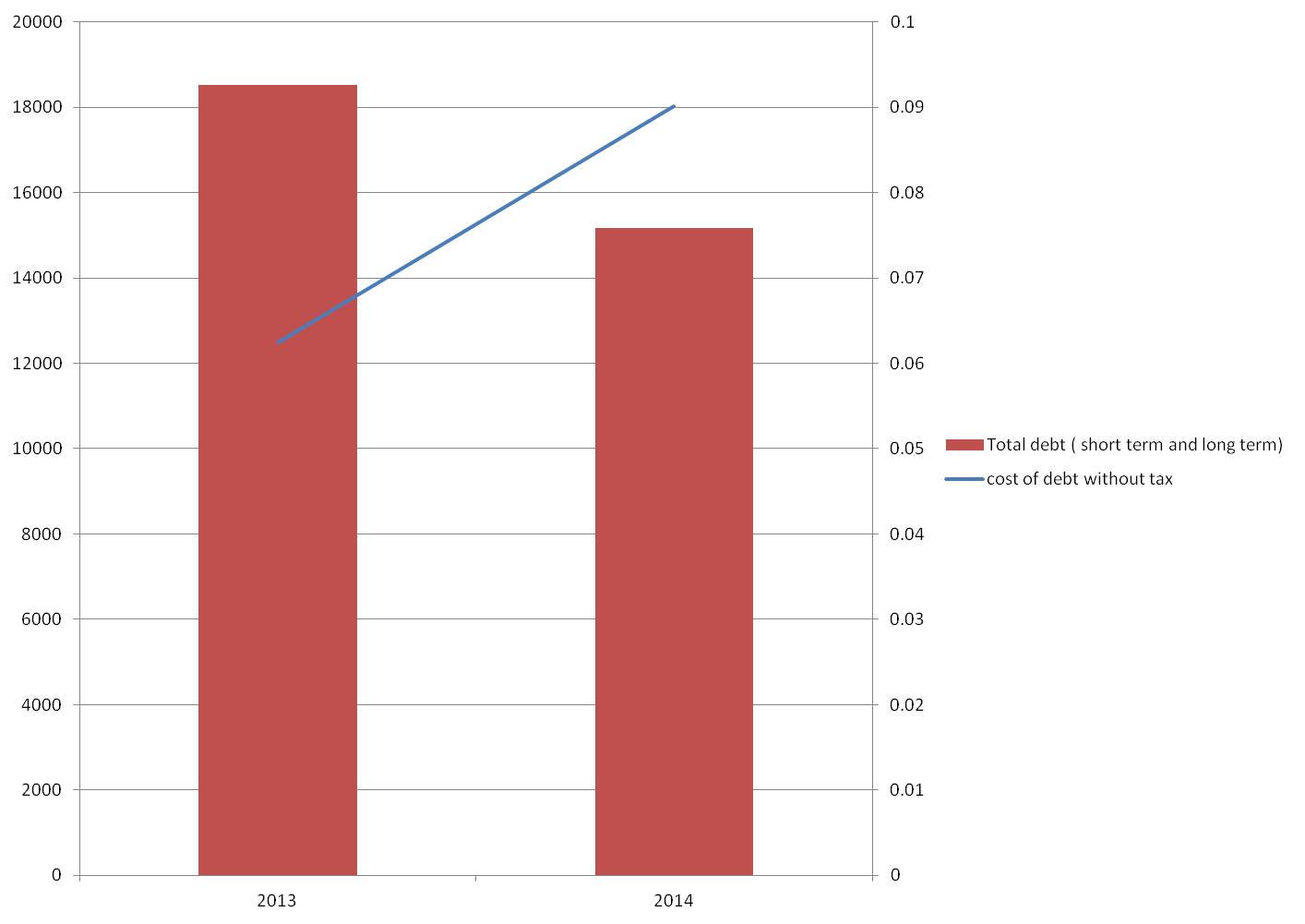

While the debt has decreased during FY14, a comparison of net worth to debt levels gives a clearer picture. The net worth has decreased 17.60 times more.

| Ratio of decrease in debt and net worth | |

| %decrease in debt | 18% |

| % decrease in net worth | 320% |

| ratio of decrease | 17.60 |

Cost of Debt

Note : cost of debt is taken without adjusting for tax as the company is earning no profits even before finance costs.

The cost of debt has sharply risen mainly due to the reason that higher rated debt had to be employed with higher risk and much lower net worth. If SpiceJet has to employ more debt it will be probably have to get at these or higher rates as risk will keep increasing with higher.

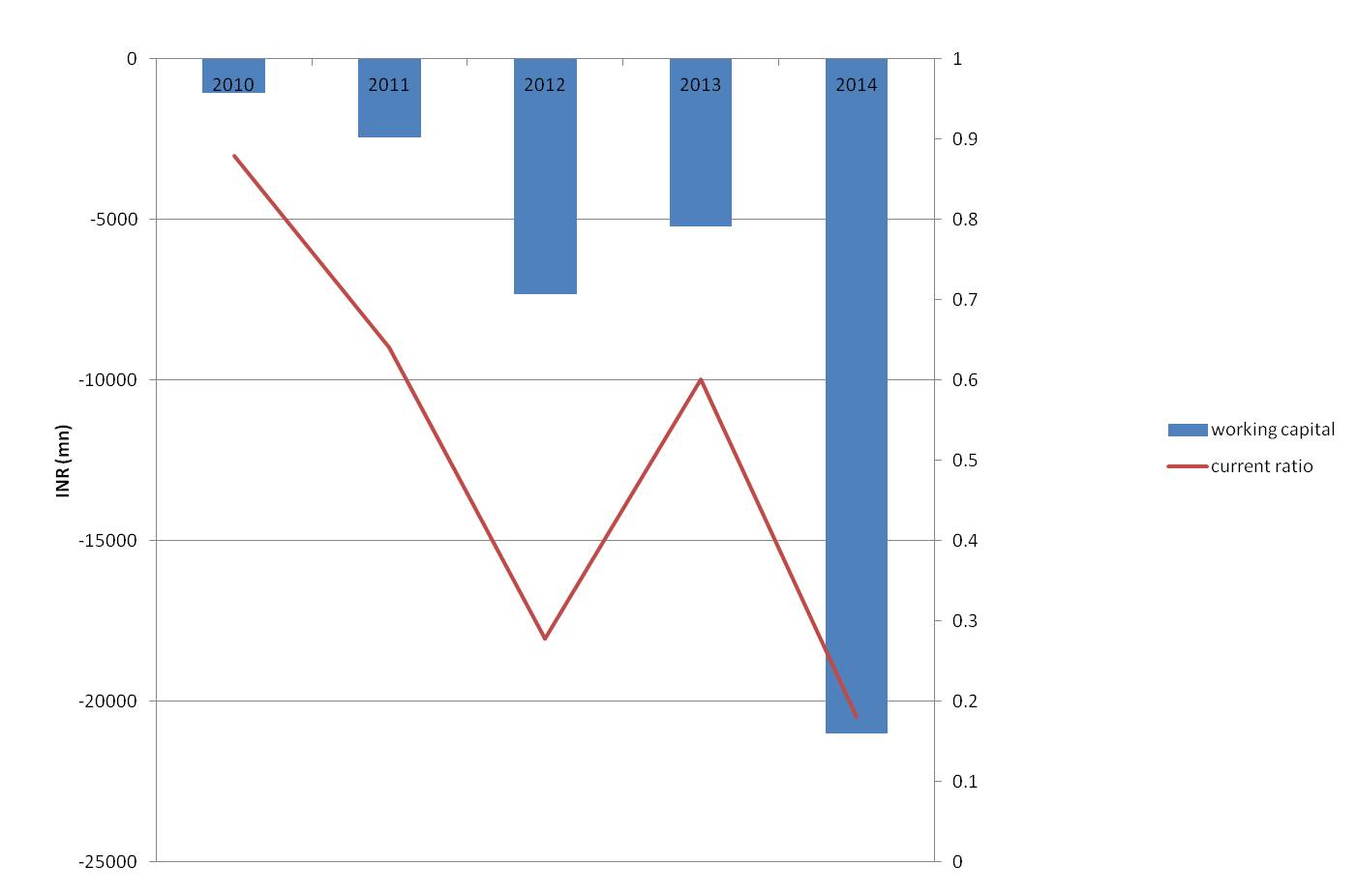

Working capital and current ratio trends

The working capital has drastically decreased in FY 14 . With low working capital levels, the company is not able to meet its current liabilities and this could point to the reason behind fare sales (which are actually a good strategy to fund working capital if managed well). Low working capital levels also has creditors starting to worry as recovery of outstanding amounts becomes challenging and is the reason why some creditors want to put the airline on a cash and carry basis.

The current ratio has come down to 0.18 . The current ratio indicates a company’s ability to service short term debt using short term assets (usually cash and credit receivables). In this case, the company has 0.18 rupees to in assets to service each rupee of debt – not quite an ideal position to be in. The company, after meeting its short term debt, will have no current assets left.

Restoring working capital levels via forward bookings

In the airline business forward bookings or advance bookings are key. This is as they allow the airline to gain cash for a service that is yet to be rendered and allow for management of inventory. Accordingly, during any situation such as a strike, pending bankruptcy or disruptions – overall strategy is aimed at restoring forward bookings in the shortest time possible. Interestingly, this was also why the Australian airline Qantas grounded its entire fleet in 2011 rather than working with uncertainty (arguably one of the most gutsy moves in aviation history).

With all the news about an airline, and cancellations once forward bookings are affected they have adverse effects. The only way to regain these is usually via fare sales especially in the low-cost segment where traffic is low yield (which is just a fancy term for leisure travelers). High yield bookings and premium bookings are not quite affected in the same way as they tend to book last minute and look at convenience (largely schedules and product offerings). Thus a business model where the traffic mix is low yield has a greater challenge in restoring forward bookings and these make a significant impact to working capital levels.

To restore working capital levels traditional methods are:

- Discounting and fare sales

- Margin improvement (generate more ancillary revenues and cut costs)

- Pricing strategy (better pricing power – but very tough given the competition)

- Generating brand strength

- A strong loyalty program (which ensures customers book)

All these moves though all except discounting are very hard to execute and manage given the nature of the industry. Discounting is great as long as costs are in line. At the end of the day, no matter how complex a business, the revenue must cover costs.

The turnaround: it is possible

A turnaround with adequate funds infusions is possible. But the patience and risk appetite of the investor would need to be high and some tough decisions are required. Any turnaround would require a complete strategic, operational and financial overhaul including collaboration by all stakeholders. A repositioning of the airline brand would be likely and the airline would likely have to decide what segments they are competing for; and equally what segments they are willing to forgo.

Any turnaround would be welcomed by investors, stakeholders and the entire aviation value-chain alike. We wish them all the best.